Featured

Table of Contents

Adjusting Home Finances in the local area During 2026

The monetary environment of 2026 has brought a new set of challenges for families trying to stabilize rising expenses with long-term stability. While inflation has stabilized compared to the start of the decade, the cumulative result on grocery rates and real estate stays a heavy burden for lots of families. Mastering the 2026 budgeting cycle requires more than simply tracking expenditures. It demands a proactive technique concentrated on credit recovery and debt reduction.Families in the local community often find that traditional budgeting techniques need adjustment to represent the present rate of interest environment. With charge card rates remaining high, the cost of bring a balance has actually become a substantial drain on regular monthly earnings. Professional guidance on Financial Wellness has assisted numerous individuals determine where their cash is leaking and how to redirect those funds towards high-impact debt payment. The initial step in this year's cycle involves a deep appearance at fixed versus variable costs. In 2026, subscription services and digital memberships have ended up being sneaky budget plan killers. A thorough audit of bank statements regularly reveals hundreds of dollars in automated payments that no longer supply value. Redirecting this recuperated cash towards charge card principals can accelerate the course to financial liberty.

Strategic Credit Reconstructing in the 2026 Economy

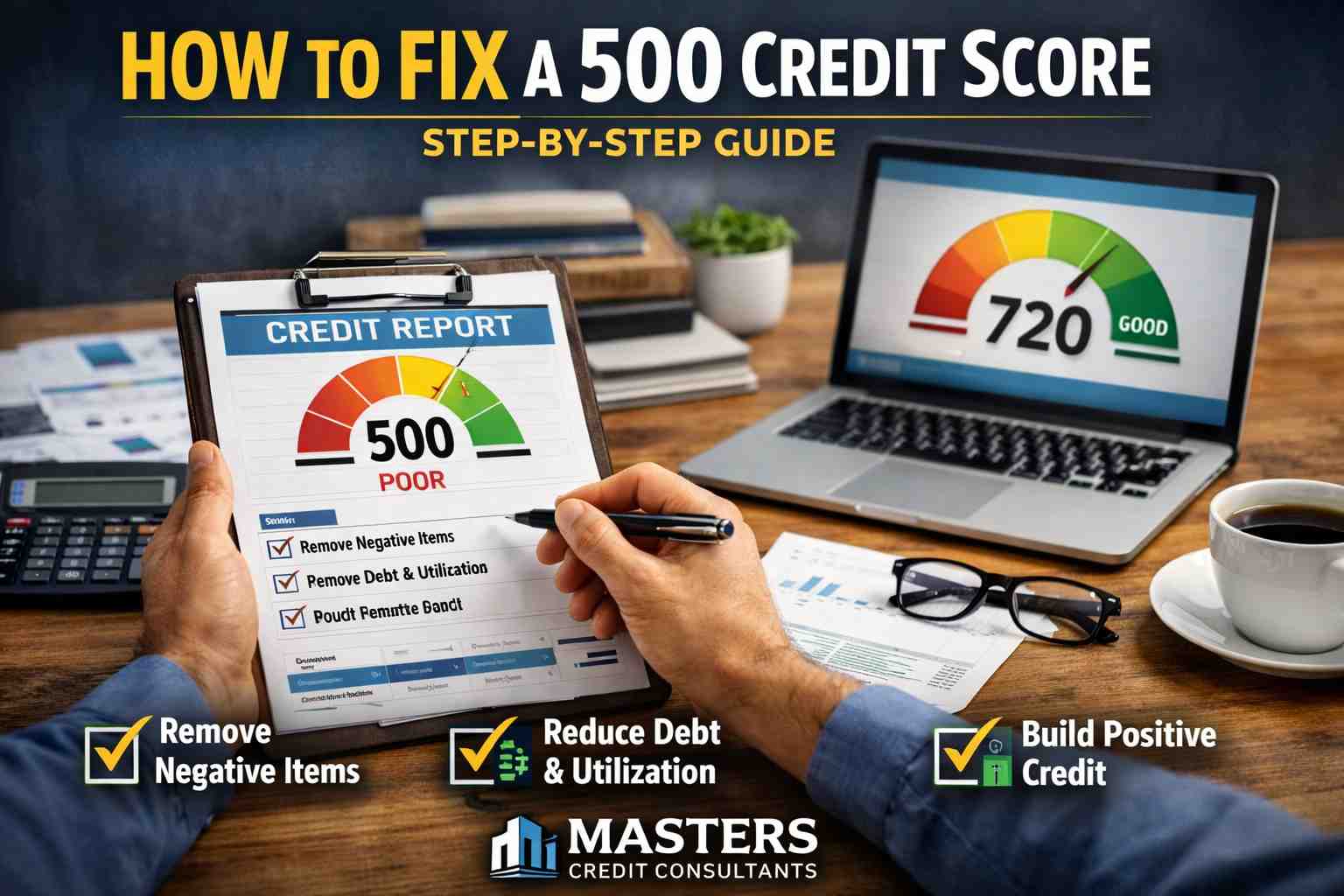

Credit history in 2026 are more than just numbers; they determine the feasibility of significant life modifications, from moving to a brand-new leasing in the surrounding region to securing a vehicle loan. Rebuilding a damaged score needs consistency and an understanding of how modern loan providers see danger. Payment history stays the most prominent factor, however the debt-to-income ratio has taken on increased significance as lending institutions tighten their requirements. Holistic Financial Wellness Programs provides a clear course for those who have experienced financial obstacles. By dealing with Department of Justice-approved agencies, households can access structured plans that streamline the recovery process. These programs often concentrate on minimizing the total interest paid, which enables more of each payment to go towards the real debt. This accelerated decrease in total balance is among the fastest ways to see a favorable relocation in a credit score.Nonprofit credit therapy firms play a crucial function in this process by providing totally free examinations. These sessions help homeowners of the regional area understand their current standing without the pressure of a sales pitch. Counselors look at the total financial photo, consisting of concealed debts and potential cost savings, to produce a roadmap that is reasonable for the 2026 expense of living.

The Mechanics of Debt Management and Consolidation

For numerous families, handling multiple credit card payments with differing due dates and rate of interest is the primary source of financial tension. Debt management programs have actually emerged as a preferred option in 2026 due to the fact that they combine these obligations into one manageable month-to-month payment. This method does more than just simplify accounting. It often involves worked out rate reductions that are not available to people acting upon their own.When a family gets in a financial obligation management strategy, the not-for-profit firm works straight with creditors to lower rates of interest and waive certain costs. This is especially helpful in 2026, where typical retail card rates have actually reached historical highs. By reducing the interest, a larger part of the monthly payment hits the principal balance instantly. This systematic method ensures that the financial obligation is paid off within a specific timeframe, usually 3 to five years.Successful budgeting likewise requires a plan for the unexpected. In the local area, families are motivated to build a modest emergency fund even while paying for debt. While it seems counterintuitive to conserve while owing cash, having a little buffer prevents the requirement to use charge card when a cars and truck repair work or medical bill occurs. This breaks the cycle of financial obligation that traps so lots of families in an irreversible state of financial insecurity.

Real Estate and Financial Literacy in the local area

Housing stays the largest expense for a lot of families in the surrounding region. Whether leasing or owning, the 2026 market requires mindful planning. HUD-approved real estate therapy has ended up being a staple for those aiming to buy their first home or those having a hard time to stay in their current one. These services supply an objective view of what a family can actually manage, factoring in the overall expense of ownership rather than just the mortgage payment.Education is the structure of any long-lasting financial success. Many community groups now use workshops on monetary literacy that cover everything from fundamental bookkeeping to complicated credit laws. Homeowners significantly depend on Financial Wellness for Idaho Families to browse intricate financial requirements and ensure they are making notified decisions. Comprehending how credit reporting works and knowing your rights under the Fair Credit Reporting Act is vital in an era where data errors can have instant monetary consequences.The 2026 budgeting cycle is not practically survival; it is about building a structure for future development. By making use of the resources supplied by not-for-profit firms, families can move from a state of consistent stress to among controlled development. This includes setting clear goals, such as reaching a specific credit history or eliminating a specific financial obligation by the end of the year.

Long-Term Stability and Neighborhood Resources

Neighborhood collaborations in the local community have broadened to provide a more detailed support group. Monetary institutions and local nonprofits are collaborating more often to provide co-branded programs that concentrate on debt reduction and cost savings. These initiatives often consist of tools for real-time budget tracking and informs that assistance households stay on schedule.Pre-bankruptcy therapy and debtor education are likewise available for those facing more serious monetary distress. These are not simply legal requirements however are developed to supply the tools necessary to avoid future financial crises. By gaining from previous mistakes and carrying out new habits, people can emerge from bankruptcy with a strategy to rebuild their credit and maintain a well balanced budget plan moving forward.The path to monetary health in 2026 is a marathon, not a sprint. It needs a commitment to altering habits and a determination to seek help when the burden becomes too heavy. With the right tools and a structured plan, households can take control of their finances and anticipate a more steady future in the United States. The resources are available; the key is taking the initial step toward a more orderly and debt-free life.

{kind=link}

Table of Contents

Latest Posts

What the 2026 Credit Laws Mean for Your State

Navigating 2026 Filing Fees in Jersey City New Jersey Debt Relief Without Filing Bankruptcy

Consumer Signals: Predatory Loaning Indications Every Debtor Must Know

More

Latest Posts

What the 2026 Credit Laws Mean for Your State

Navigating 2026 Filing Fees in Jersey City New Jersey Debt Relief Without Filing Bankruptcy

Consumer Signals: Predatory Loaning Indications Every Debtor Must Know